Validation · last 7 days

Results.

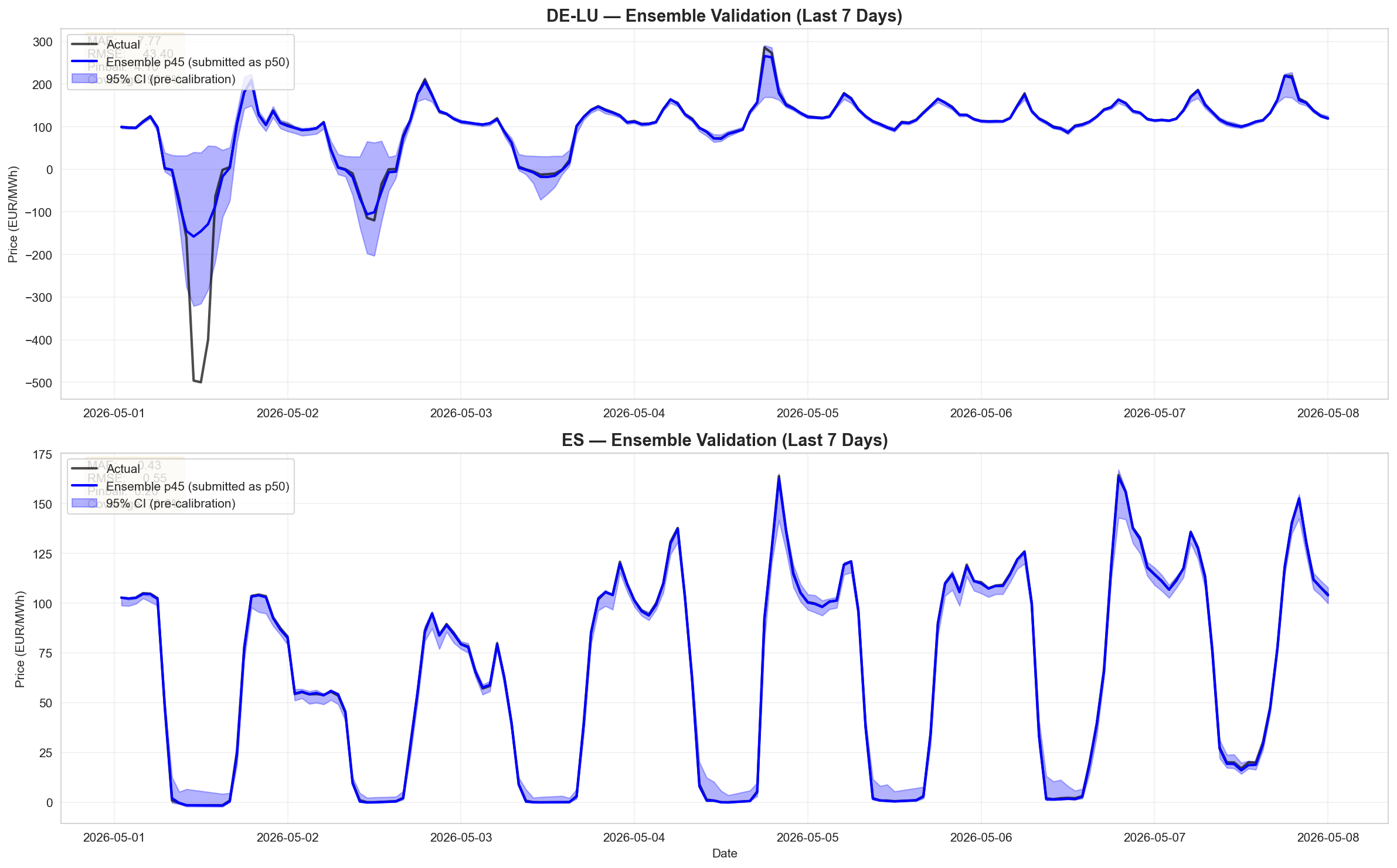

95% interval coverage in both zones — ES is an order of magnitude tighter than DE-LU.

DE-LU · gas-coupled

Pinball Loss · q 0.45

0.00

EUR/MWh

MAE8.1

RMSE42.15

Coverage95%

ES · solar-saturated

Pinball Loss · q 0.45

0.00

EUR/MWh

MAE0.38

RMSE0.65

Coverage95%

ES is cleaner — solar dynamics are more predictable. DE-LU's pinball is carried by a single rare spike day.

95% Coverage · Both Zones

— Actual

— Ensemble p45

— 95% CI band